Most Realtors don’t know this

Most Realtors don’t know this formula, and their clients pay the price!

Although every lender knows this formula, because Realtors don’t know it, they’re not writing contracts that can best leverage today’s market to reduce the affordability for their buyers.

The question is “how many closing costs can a seller pay?”

*Disclaimer: this data is subject to change. It’s our responsibility to educate our clients and get them in front of mortgage professionals.

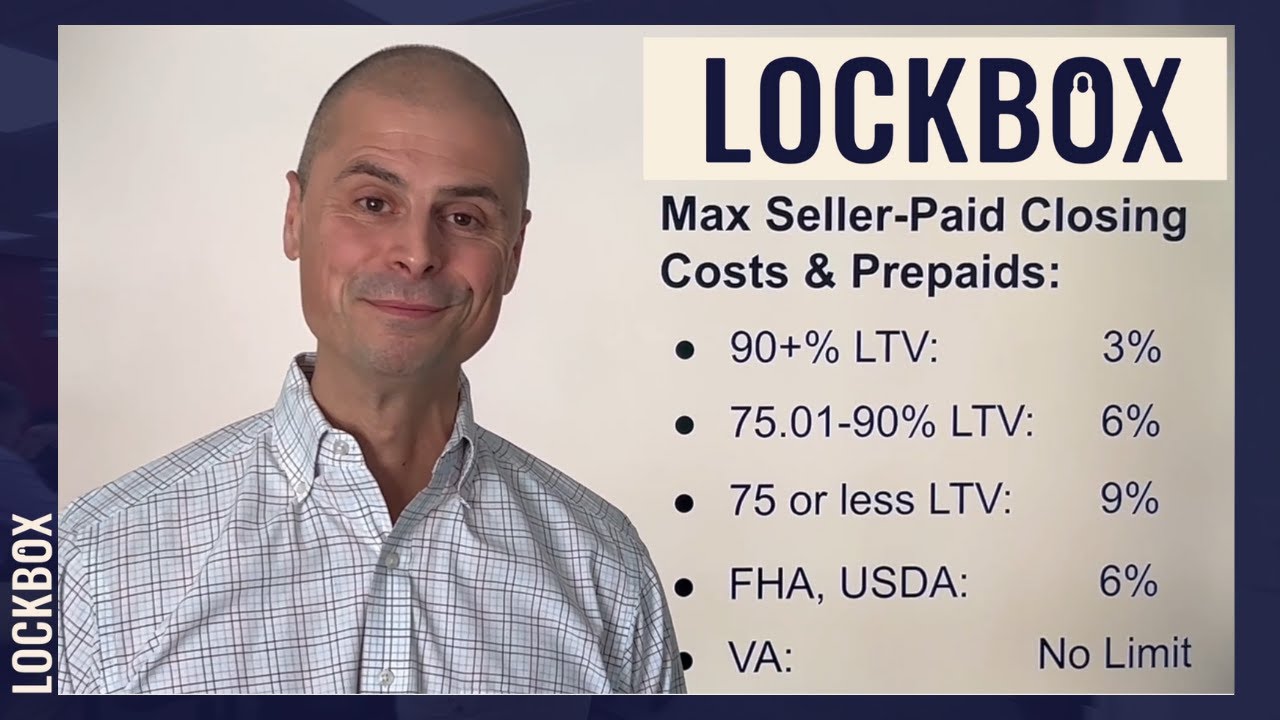

Here’s the formula that lenders use for conventional mortgages, where the buyer is putting less than 10% (the loan to value ratio is 90 or more). Conventional mortgages will allow the seller to pay up to 3% of the purchase price as seller paid closing costs and prepaids for the buyer.

Quick example: on a $200,000 deal, the seller can pay 3% or up to $6,000 in closing costs and prepaids. This is where it gets interesting. If your client is putting 10-25% down on their home, the seller can pay up to 6% of the purchase price in prepaids and closing costs. On a $200,000 loan, that’s $12,000. You can do a ton of rate buy down with that much money!

Now if your client is putting more than 25% down, the seller can pay up to 9%. That would be $18,000 on a $200,000 purchase – that’s a lot of money!

Let’s look at federal government loans. For FHA and USDA, 6% is the maximum amount of seller-paid closing costs. Again, on a $200,000 purchase on an FHA or a USDA loan, you can have up to $12,000.

Remember, the average 3-2-1 loan requires only about 4% in seller-paid closing costs, so there’s more than enough room here for your government loans.

This is the whopper: there is currently no limit on seller-paid closing costs on VA loans. That’s a massive opportunity.

When you are equipped with this information, you can empower your clients to make offers that get accepted at interest rates that they’re comfortable with in today’s market.