Interest Rates: A Crash Course for Realtors

Over the past 5 months, Lockbox has posted primers in the economics that drive our industry. Today’s subject is interest rates: how they are determined and how they impact the residential home sales industry.

The Basics: Federal Funds Rate

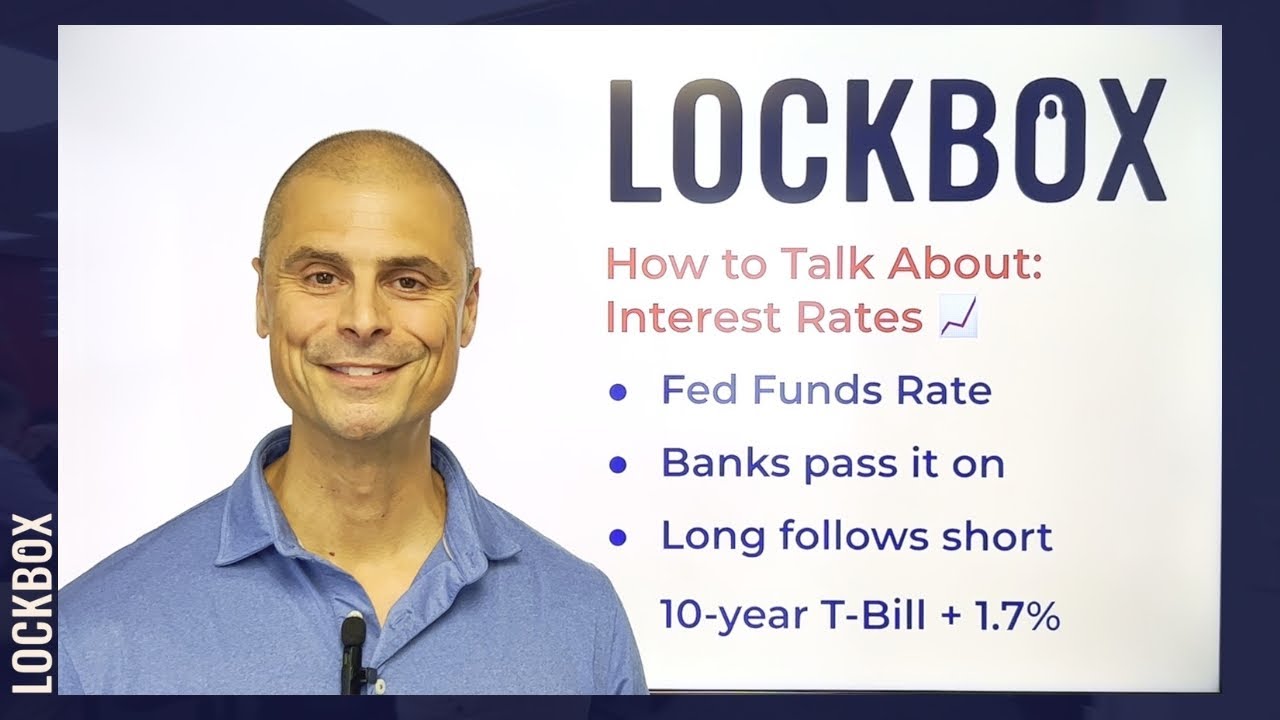

In a previous blog post, you learned about the importance of the Federal Funds Rate. As a refresher, it’s the rate the Federal Reserve sets at which banks can lend money to each other, and how the federal government lends to those banks. What you need to recall from that post is that when the federal funds rate goes up, banks need to pass that increase in the expense of money along to their end user: the consumers or businesses borrowing money. So, as this rate increases, the interest rates offered by banks to businesses and consumers will follow suit.

Short-term vs. Long-term Interest Rates

The Federal Funds Rate impacts the short-term rates that banks lend to each other. But those are ultimately overnight rates that are set. Historically, when there’s a sustained uptick in those short-term interest rates, it eventually begins to influence long-term interest rates. Conversely, if short-term interest rates begin to drop in a sustained fashion, long-term rates historically follow suit. This cause-and-effect relationship is essential to understand, especially when dealing with 30-year mortgages.

Enter the Federal Ten-Year Treasury Bill

This might surprise you, but the 30-year mortgage rate isn’t directly set by the federal funds rate. Its primary influencer is the Federal ten-year treasury bill, a shining beacon in the investment world due to its stability and low risk. The federal funds rate does have an indirect impact on the 10-year treasury bill. Historically, the 30-year fixed mortgage rate is – on average – about 1.7% higher than the ten-year treasury bill rate. This increase in interest rate is to offset the additional level of risk that investors take on when they buy mortgage debt (effectively, consumer debt) vs US Federal debt (considered some of the safest debt to buy on the planet).

The Big Picture

So here’s how it all works together: Banks lend money to each other at the Federal Funds Rate. As this rate rises, so do the rates banks offer to their clientele. With time, these short-term interest rate changes impact long-term changes. The federal ten-year treasury bill, a reliable and relatively risk-free debt instrument, plays a pivotal role in determining mortgage rates. Given the inherent risk in mortgages (consumer debt vs the United States government debt), there’s typically a 1.7% higher rate, or risk premium, than the treasury bill.

For instance, if 10 year T Bills are at a 5.3% interest rate, then mortgage rates, at their average historic premium over T Bill rates, would be around 7%.

It’s All About The Economy

Effectively, the Federal Reserve uses its Federal Funds Rate to influence interest rates in sectors across the country – from credit card debt to corporate bonds to consumer mortgages. If the Federal government wants to cool off a hot economy, it may raise its Federal Funds Rate, making borrowing and spending more expensive. And if the economy is in recession or stagnating, the Federal Reserve may lower its Federal Funds Rate to stimulate spending and investment. This rate indirectly impacts the 10-Year T-Bill, and ultimately, the interest rate your client is quoted for their mortgage.

Armed with this knowledge, you’re poised to offer your clients a deeper understanding of mortgage rates. If your client asks, “How are mortgage rates calculated?” you’re now ready with an insightful answer!